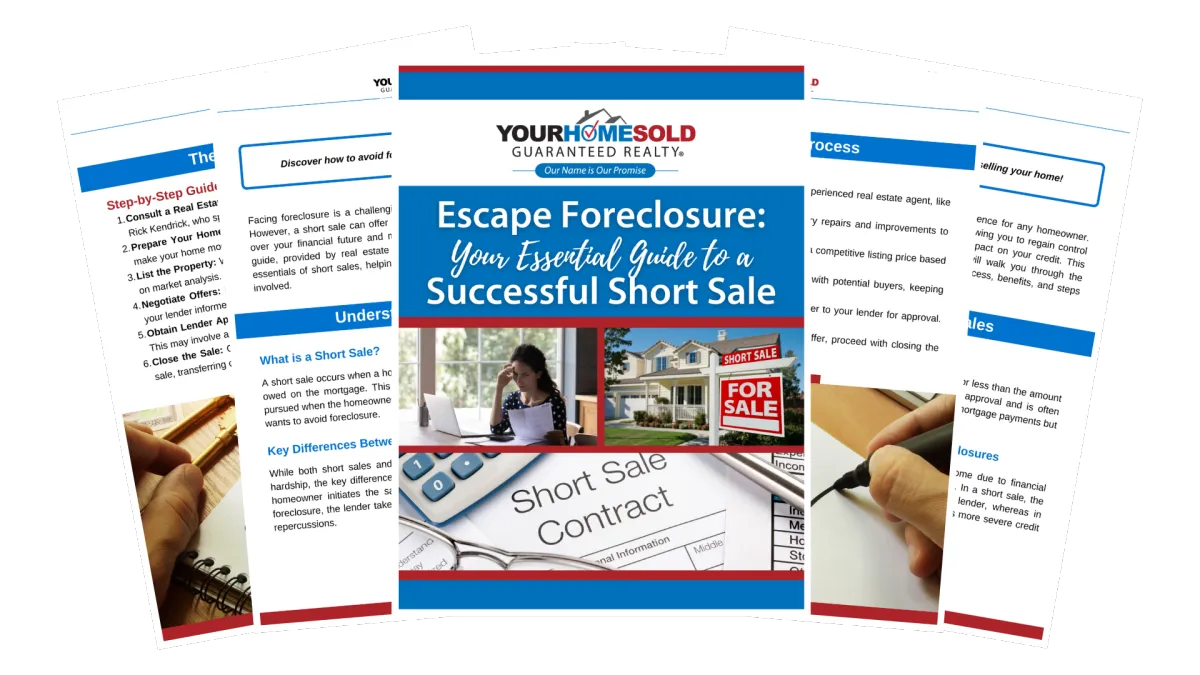

Escape Foreclosure: Your Essential Guide to Successful Short Sales

How to Qualify for a Short Sale in Palm Beach County, Florida

Navigating the complexities of a short sale can be challenging, particularly in competitive markets such as Palm Beach County, Florida. This guide provides a comprehensive understanding of short sales, including their definition, purpose, and the essential steps for qualifying and preparing your finances.

It outlines the short sale process, identifies potential challenges, and offers strategies for achieving success. Whether you are a homeowner contemplating this option or a buyer seeking opportunities, this guide will furnish you with the knowledge necessary for well-considered choices.

Understanding Short Sales

Understanding short sales is essential for homeowners in Palm Beach County, Florida, particularly for those experiencing financial hardship and contemplating alternatives to foreclosure. A short sale entails selling a property for an amount that is less than the outstanding mortgage balance, enabling homeowners to reduce their debt and circumvent the prolonged foreclosure process.

This approach can offer substantial debt relief and present a more manageable means of addressing difficult financial circumstances, thereby serving as a viable solution for individuals struggling with their mortgage obligations.

If you are a homeowner or potential seller needing more information about short sales, don't hesitate to schedule a consultation with our experts. Book your appointment here or call/text Rick Kendrick at 561-508-8453.

Definition and Purpose

A short sale in real estate refers to the process in which homeowners sell their property for an amount that is less than the outstanding mortgage balance, contingent upon the lender's approval, in order to avoid foreclosure. This option often becomes appealing when homeowners experience financial distress due to unforeseen circumstances such as job loss, medical expenses, or other economic challenges.

The prevailing trend of declining property values can further exacerbate their situation, resulting in limited equity and increasing debts. Consequently, pursuing a short sale can serve as a viable solution to alleviate the potential risk of foreclosure, offering both relief from financial obligations and an opportunity to negotiate with lenders for a more manageable resolution.

In many instances, homeowners may also benefit from an expedited sale process, enabling them to transition into new housing arrangements without facing the prolonged consequences of foreclosure on their credit history.

Qualifying for a Short Sale

To qualify for a short sale, homeowners must meet specific financial criteria, which include demonstrating a legitimate financial hardship that affects their capacity to maintain mortgage payments.

Financial Criteria and Requirements

The financial criteria for qualifying for a short sale typically encompass the provision of proof of income, documentation of financial hardship, and an assessment of the homeowner's total debt obligations. To substantiate these requirements, homeowners are generally required to submit recent pay stubs, tax returns from the preceding two years, and current bank statements that accurately reflect their financial status.

These documents play a vital role in providing lenders with a comprehensive understanding of the homeowner's income stability and spending behaviors. By analyzing this information, lenders can evaluate the homeowner's capacity to fulfill their financial obligations and ascertain the authenticity of their hardship. This thorough examination is essential for making informed decisions, determining whether a short sale is a feasible option, and ultimately facilitating a more efficient process for all parties involved.

Facing financial difficulties and considering a short sale? Schedule a consultation with Rick Kendrick to explore your options. Book your session now or reach out directly at 561-508-8453 via call or text.

Steps to Take Before Applying for a Short Sale

Before submitting an application for a short sale, homeowners should undertake essential preparatory measures. This includes compiling the necessary financial documents and seeking the expertise of a qualified real estate agent who specializes in short sales, in order to navigate the process effectively.

Preparing Financial Documents

Preparing financial documents is an essential step for homeowners pursuing a short sale, as lenders necessitate comprehensive documentation to evaluate their financial hardship. This process typically includes the submission of proof of income, such as recent pay stubs or tax returns, which assists the lender in assessing the homeowner's financial stability.

Additionally, expense reports detailing monthly expenditures can offer valuable insights into the household's financial situation. It is crucial for applicants to provide evidence of financial hardship, such as medical bills or unemployment notices, to fortify their case.

Thorough documentation is vital in the approval process, as incomplete or inaccurate information may result in delays or rejections. Therefore, it is imperative that all submitted materials are precise and accurately represent the individual's current financial circumstances.

Consulting with a Real Estate Agent

Consulting with a knowledgeable real estate agent is essential for homeowners considering a short sale. Such professionals provide valuable guidance on market trends, pricing strategies, and negotiation tactics that can significantly enhance the chances of lender approval.

Their expertise is crucial in navigating the complex landscape of lender negotiations, which can often be overwhelming for individual sellers. An experienced agent possesses the skills necessary to communicate effectively with lenders, securing favorable terms and alleviating much of the stress associated with the short sale process. Additionally, they can implement targeted marketing strategies to attract potential buyers, ensuring that the property is presented in the most advantageous manner.

By managing all aspects of the sale, these professionals not only increase the likelihood of a successful transaction but also strive to expedite the process, ultimately providing peace of mind for homeowners facing challenging financial circumstances.

Understanding the complexities of short sales can be challenging. For personalized guidance and expert advice, schedule a consultation or call/text Rick Kendrick at 561-508-8453.

The Short Sale Process

The short sale process encompasses several essential steps, including obtaining lender approval, effectively marketing the property, and negotiating offers. Each of these components can have a considerable influence on both the timeline and the overall outcome of the transaction.

Timeline and Key Players Involved

The timeline for a short sale can vary significantly depending on the cooperation of key stakeholders involved, such as the homeowner, lender, potential buyers, and prevailing local market conditions. The process typically commences with the homeowner gathering the necessary documentation, which may take several weeks to complete.

Following this, once the lender reviews the application, the approval or denial of the short sale request can take anywhere from 30 to 90 days. Real estate agents are instrumental during this process, as they are responsible for marketing the property and identifying interested buyers.

This phase can extend over several months, contingent upon buyer interest and the negotiation process. Ultimately, effective communication among all parties is essential for facilitating a smoother transaction and can considerably impact the overall timeline of the short sale process.

Potential Challenges and Solutions

Potential challenges in the short sale process may arise at various stages, particularly during negotiations with lenders. However, a comprehensive understanding of these issues can assist homeowners in navigating the process more effectively.

Dealing with Lenders and Negotiating Terms

Engaging with lenders and negotiating terms is a critical component of the short sale process, as homeowners must effectively communicate their financial hardships to obtain the necessary approval. A clear and articulate presentation of their circumstances can significantly impact the lender’s willingness to consider their request.

Homeowners should highlight their unique situations by providing comprehensive documentation, including income statements and evidence of financial distress, thereby demonstrating the need for leniency. By constructing a compelling case, they not only substantiate their claims but also strengthen their negotiating position.

Understanding seller rights and appropriately invoking those rights can further enhance negotiations. Utilizing strategies such as setting realistic expectations and maintaining open communication can improve the likelihood of securing favorable terms during this complex approval process.

Tips for a Successful Short Sale

To achieve a successful short sale, homeowners should implement best practices and strategies that increase the likelihood of lender approval and facilitate an expedited sale process.

Best Practices and Strategies

Implementing best practices and strategies can substantially enhance a homeowner's prospects of achieving a successful short sale, particularly in a competitive real estate market such as Palm Beach County. Homeowners aiming to maximize their sale potential should consider several key approaches. One effective strategy involves pricing the property competitively; an attractive price point can attract more prospective buyers and generate a sense of urgency in the market.

Additionally, understanding local market trends is essential; awareness of optimal listing times and familiarity with comparable sales can significantly influence outcomes. Offering buyer incentives, such as covering closing costs or providing home warranties, can increase the property’s appeal and facilitate quicker sales. By integrating these strategies, homeowners can achieve a more favorable outcome in any short sale situation.

If you need more details or wish to discuss your situation with a specialist, schedule a consultation with us. Book an appointment or contact Rick Kendrick at 561-508-8453 via call or text for immediate assistance.

Frequently Asked Questions

What is a short sale and how do I qualify for one in Palm Beach County, Florida?

A short sale is a real estate transaction where the homeowner sells their property for less than the amount owed on their mortgage. To qualify for a short sale in Palm Beach County, Florida, you must be experiencing financial hardship and be unable to pay your mortgage.

What is considered a financial hardship when applying for a short sale in Palm Beach County, Florida?

Financial hardships can include job loss, divorce, medical emergency, or any other situation that has significantly impacted your ability to pay your mortgage. It is important to provide documentation to support your hardship when applying for a short sale.

Can anyone qualify for a short sale in Palm Beach County, Florida?

No, not everyone will qualify for a short sale. Lenders will evaluate your financial situation and determine if a short sale is a feasible option. They may also require you to attempt other options, such as loan modification, before considering a short sale.

Is it better to pursue a short sale or simply allow my Palm Beach County, Florida home to go into foreclosure?

In most cases, it is better to pursue a short sale rather than letting your home go into foreclosure. A short sale can help you avoid the damaging effects of a foreclosure on your credit and may also result in a more manageable outcome for your lender.

What steps should I take to qualify for a short sale in Palm Beach County, Florida?

To qualify for a short sale, you should first contact your lender and explain your financial situation. They will likely require you to provide documentation of your hardship and may also request a short sale package. It is important to work closely with your lender and a qualified real estate agent throughout this process.

How long does it take to qualify for a short sale in Palm Beach County, Florida?

The timeline for the short sale process can vary depending on the complexity of your situation and the responsiveness of your lender. In general, it can take several months to complete a short sale in Palm Beach County, Florida. It is important to be patient and work closely with your lender and real estate agent to ensure a successful outcome.

We’ve Created A Beginner-Friendly Guide To Help Your on Your Path to Financial Recovery

Unlock the secrets to navigating financial distress with "Escape Foreclosure: Your Essential Guide to Successful Short Sales." This comprehensive guide empowers homeowners with the knowledge and strategies needed to navigate the complexities of short sales effectively. Whether you're seeking to minimize credit impact, regain control over your financial future, or explore options for debt forgiveness, this guide provides step-by-step instructions and expert insights to help you successfully navigate the short sale process. Don't let foreclosure define your financial future—take charge with the essential tools and guidance offered in this indispensable resource.

© Copyright

2024.

Your Home Sold Guaranteed Realty of Florida. All rights reserved.

2022 All Rights Reserved.